Many people know they should have life insurance but put off getting it because they feel overwhelmed. How much should you get and how do you know which type to buy? A good financial/ insurance advisor’s job is to help you answer those questions. Often people spend more time planning their vacations than they do their financial future despite the importance of the latter. Premature death or disability can derail your personal and retirement objectives if not planned for in advance.

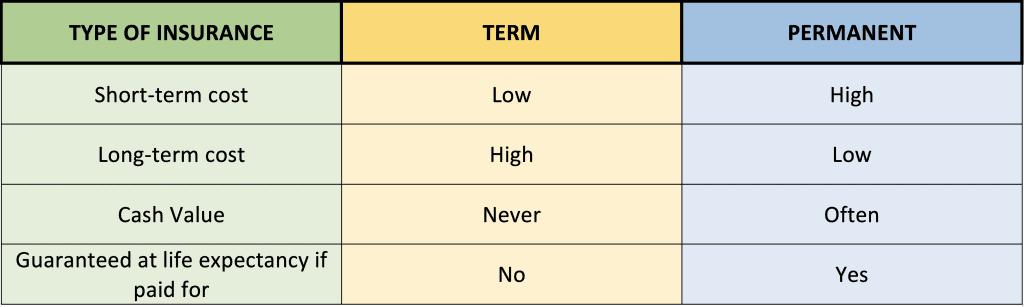

In general, there are two types of insurance – term (you rent it) and permanent (you own it). Much like real estate, there are pros and cons to both. As with rent, term insurance premiums increase over time and will often become too expensive in the future. Insurance is priced based on the level of risk the insurance company is taking on. As you age, the risk increases as do the premiums. Therefore, if you need insurance in the short-term (for 10 years for example), term insurance will be much less expensive — because the insurance company is assuming it is a lower risk for something to happen to you in that time. Conversely, permanent insurance will have to pay out eventually because the mortality rate for all of us is 100%.

Permanent insurance is an asset that you own. Depending on how it is set up, the premium will stay the same regardless of how old you are (its based on your age at the time the policy is issued) but the death benefit may increase. This helps to offset inflation as your purchasing power will likely be reduced by the time your dependents are making a claim (think about groceries costing more now than they did 20 years ago). There is also a provision in many policies where the policy accumulates what is known as a cash value. Depending on the terms of the policy, this will likely allow you to access some of the cash value of the policy during your lifetime.

When you’re deciding what kind of insurance to get, a good starting point is to ask yourself what the insurance is intended to do. Do you need it to last your lifetime or only a specific time (e.g., to cover a 20 year mortgage), will you need it to cover off other debts, replace your income, send your children to university, cover final expenses including your funeral, etc.?

Consider Carol and John. They have three kids, a home, a cottage which has appreciated in value since they bought it and various investments. All children are under the age of 15. Carol and John want to ensure that their mortgage is paid off if one of them dies p r e m a turely. They also want their kids to inherit their cottage without having to pay a large tax bill. They would like to fund their children’s post-secondary education in the event they are not around to pay for it. It is important to them that the survivor can meet their current financial obligations in the case one of their incomes ceases due to death.

The mortgage and schooling are both short-term expenses. Eventually, Carol and John will not need the insurance anymore as the mortgage will be paid off and the kids will have finished their schooling. Therefore, term insurance would likely be the appropriate choice to cover these expenses.

Regardless of how long they live, their cottage will trigger a taxable event upon the second death. The tax will be equal to the capital gains rate (currently 50%) multiplied by the increase in value since they purchased the property. For example, if the cottage was purchased for $200,000 and is valued at $400,000 at the time of death, this would trigger a $100,000 tax bill. Their funeral expenses will also apply regardless of age. Income replacement to help pay bills in the event one of them outlives the other will continue regardless of when death occurs but the amount needed will change depending on how far into their working career or retirement they are. For these reasons, permanent insurance would likely be used for these items. The income replacement may be a combination of term and permanent insurance.

Regardless of the combination of insurance Carol and John’s advisor helps them select, meeting their immediate and long-term needs is easy with one application.

Throughout your lifetime, your needs and obligations will change. For this reason, it is important to review your plan on a regular basis and update it as needed. You should meet with your advisor for an annual review or as you experience a life change (i.e. you get married or divorced, have a child, change your job etc.). As Lewis Carroll said, “If you don’t know where you’re going, any road will get you there.” In order to get where you would like to go, creating an intentional roadmap is vital. A sound financial plan reviewed regularly with the help of a competent financial advisor will help you stay on track to reach your goals with peace of mind.

Published in the BCNA Bulletin, Spring 2020

This article has been provided by Saskia Vermeulen, Southlands Financial and Sindy Billan, SB Wealth Solutions* and is for informational purposes only. It is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Information obtained from third parties is believed to be reliable, but no representation or warranty, express or implied, is made by Sindy Billan or Saskia Vermeulen as to its accuracy, completeness or correctness.

*SBILLAN Wealth Solutions Inc. doing business as SB Wealth Solutions E&O/E 2019